By M. Snarky

Dear Governor Newsom,

As a native California son, please, for the love of God…wait…make that, for your love of inappropriate meals during the COVID-19 lockdown at ultra-bougie The French Laundry, and your love for extra-marital affairs with the wife of a close friend, please give us Californian’s a gas tax break. We’d love that.

Outside of one of your hand-picked focus groups, I want to know if you have ever personally talked to the average working men and women on the street about their ever-increasing gas tax burden. It doesn’t seem like it because it appears to me that you’re more of a pollster guy who prefers not to get any face time with the general public by design because you might breakdown and cry if someone yells at you.

It is my understanding that if the California Air Resources Board (CARB) gets their way, they’re going to add an additional (estimated) $0.54 cents per gallon excise tax to the already exorbitantly high $0.612 state tax and fees which will add up to a total of $1.152 per gallon in gas taxes alone, the most expensive in the country. While most states are paying around $4 per gallon, we’re paying over $6 per gallon.

I don’t believe that we should be aiming for or be proud of being #1 in the highest gas tax in the nation. I strongly recommend that we go for being #1 in something else, for example, the lowest gas taxes of any state.

You see, it feels as if Sacramento is intentionally inflicting financial pain on all of us in the working class in this state in a perverse the end justifies the means because fossil-fuel is evil scheme. We have this tremendous amount of crude oil directly under our feet—a natural resource, by the way—yet the California legislature and CARB are ostensibly outlawing it with their overt attempt to force everyone into an electric vehicle under a socially engineered extensively complicated cap and trade program in a collective effort to reduce CO2 emissions for a very lofty—yet self-imposed—2045 carbon neutrality goal. Who asked for this anyway? Oh, that’s right; the K Street Cabal did.

I’d like to see an environmental impact study of the environmental impact study that was used to underpin this carbon neutral objective. I’ll bet the carbon emissions from the CARB members alone are stratospheric, and probably mostly consists of methane and hot air.

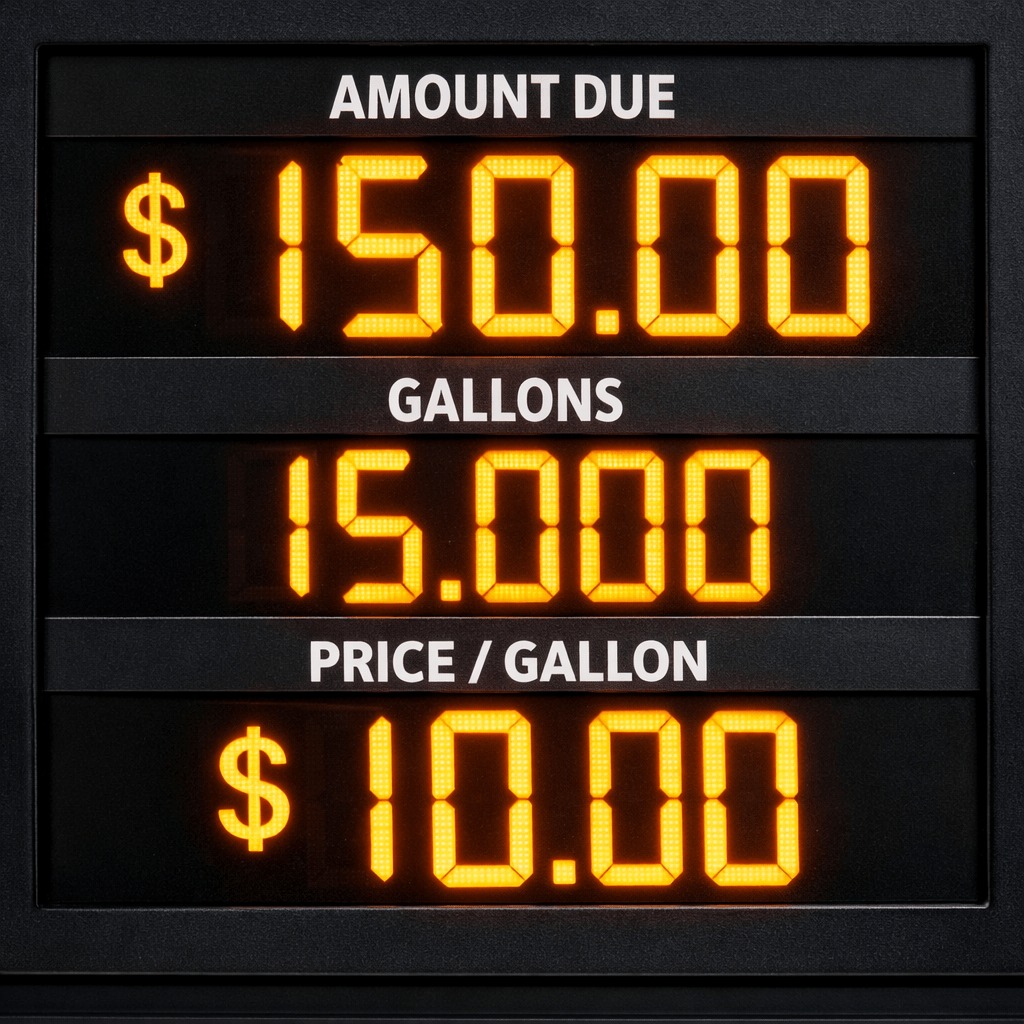

It seems like the state is betting that when gasoline hits an outrageous price, say, $10 per gallon, people will be forced into selling their fossil fuel burning internal combustion engine cars—because now it costs them $150 for a weekly fill-up—and buy an expensive EV, which, by the way, have their own significant negative environmental impacts. I won’t bore you with the facts here, but you can Google them later.

In the state’s twisted logic, they’ll tell us that instead of spending $650 a month in gasoline, now we can afford a monthly EV payment. They’ll even expect us to pat them on the back for the “favor,” and thank them for saving the environment. It reminds me of this quote from Harry Browne, “The government is good at one thing. It knows how to break your legs, and then hand you a crutch and say, ‘See if it weren’t for the government, you wouldn’t be able to walk.’”

By the way, not everyone can afford to drive a plush Rivian R1S like you do, which costs between $77K-$125K. Oh, snap! It’s the CHP Dignitary Protection Section that paid for your fancy Rivian EV’s (indeed, I’m aware that there are two of them in your li’l fleet). Isn’t the CHP funded by the state budget? Doesn’t the money for the state budget come from the taxpayers? I can smell the sickening stench of the hypocrisy emanating from Sacramento all the way down here in Southern California. The disdain that Sacramento holds for the taxpayers in this state is palpable.

I’ve read reports which note that the California power grid isn’t even ready for the EV revolution because it is insufficient and will need between $6 billion and $20 billion invested by 2045 to upgrade transmission lines and local distribution systems to handle the increased electric demand for EV charging.

Currently, there are only about 1.25 million EVs registered in California (out of 36 million cars in total), so even if you doubled this to 2.5 million EVs and go with a middle-of-the-road $13 billion construction price tag estimate, the per EV cost for the grid upgrades would be $10,400 before the usual cost overruns. Seems expensive to me, and I’m not convinced this is how tax dollars should be spent, but I’d bet $13 billion that the labor and trade unions and special interest groups are fully behind it.

Ironically, you have shut down all but one of the nuclear power plants in the state, and statistically speaking, nuclear power is one of the cleanest on-demand power sources on the planet, so there’s that. What is also ironic is that 35% of the state’s electricity comes from natural gas fired steam turbine driven generators, and the last time I checked, natural gas is a petroleum product. I guess you’ll have to shut those down too while you’re at it. I’m sure the people will get used to the flickering lights and rolling blackouts over the next 25-years of grid improvements for the sake of progress. What a stunning, state mandated conundrum we find ourselves in.

Did you not know that some of your favorite Dippity-Do hair products have petroleum-based ingredients? I guess you’re going to be forced to change your hair product brand to something that is carbon neutral. I hope you find something with a hold that is as equally stiff as your political ideology.

I know that we’re just the little people who are several degrees of separation outside of your elitist-multi-millionaire-handsome-guy-surrounded-by-an-entourage-of-yes-men-and-women bubble; but we’re the ones that actually pay for the super pricey high-speed rail to nowhere and multi-billion-dollar carbon neutrality projects, et. al., plus all the other “free” stuff you hand out like it was Halloween candy bought in bulk from Costco. We’re also the one’s that will never see the inside of a restaurant like The French Laundry, unless of course we get an invitation from the governor’s office.

Lately, you’ve been jetting around the country promoting your memoir and talking about how great your governance of the Golden State has been, but didn’t California slip from the 4th to the 5th largest economy under your watch? Maybe your dyslexia got that mixed up and you thought we went up to 4th from 5th. Just guessing. Isn’t California also ranked as the #1 state in net domestic migration loss over the last few years? In lay terms, this means that more people have left the state (bad!) than are coming to the state (good!). It’s math.

What about some notable large companies leaving the state like Tesla, Chevron, X/Twitter, Oracle, SpaceX, McKesson Corp, Toyota Motor North America, and now Yamaha Motor Corporation USA? In case you haven’t read the news, they have left or are leaving California for the same reasons, which are high operating costs, burdensome regulations, and high taxes. Don’t get me started on the Hollywood Exodus, or the outrageous one-time billionaire tax scheme—they’ll leave the state too.

I’m sure the ultimate plan to replace all of that lost tax revenue is to increase taxes on everyone else which is business-as-usual in Sacramento, but I think we’re tapped out. Perhaps you could try something totally radical, like cutting spending. You’re laughing out loud now, but it’s definitely not a bad idea. Maybe audit all of the spending programs too. I’m sure the state controller can find some money lying around. What’s that? Oh, that’s right, you’re not funding the state controller’s office, ergo, there are zero audits happening. If the controller isn’t monitoring the inflow and outflow, then who’s watching the money. Is it a guy named Ponzi?

Governor Newsom, the high taxes, population flight, and business departures aren’t business-as-usual; these are extremely alarming and largely self-inflicted wounds via toxic over-governance. You should be deeply concerned and losing sleep over these trends and, I don’t know, maybe doing something serious to reverse them. I know you have higher office aspirations, but you are technically the sitting governor of California until January of 2027, and you can surely do something.

You recently stated during your book tour that you can’t read speeches because of your dyslexia. By extension this also infers that you cannot (or do not, or worse, will not) read legislation either, which is very troubling. Getting a ten-minute verbal bullet point summary on a piece of legislation that is perhaps dozens (or hundreds) of pages long delivered to you by an aide is not the equivalent of reading the entire text, which is often where the devil resides. Indeed, the devil is always in the details, but I suppose that this is how the sausage gets made in Sacramento, regardless of the high cost, foul smell, and unpleasant taste.

The big whopper is how did the state go from a $97.5 billion budget surplus in 2022 to a $2.9 billion (estimated) deficit by 2026 during your term as governor? This is a massive $100.4 billion financial loss in four years. Bernie Madoff went to prison for less than this. Where did all of that money go anyway? I wonder how many degrees of separation there are between you and the recipients of all that money. Five? One? Zero?

If this gargantuan loss of money happened to a portfolio manager, or a banker, or a brokerage, he/him, she/her them/they would be arrested and promptly find themselves under an FBI investigation for wire fraud, mail fraud, corruption, embezzlement, money laundering, malfeasance, etc. These are just the legal formalities prior to a definite conviction and subsequent long prison sentence. Madoff was sentenced to the maximum of 150 years in federal prison for his infamous $65 billion Ponzi scheme. I wonder how much time a governor would get for “losing” $100.4 billion.

Maybe we should change the name of the state to Corruptifornia?

I’m sure that you have a regurgitated word salad explanation for all of this, but everyone knows that not one single good story has ever started with a salad, not even one that is served up properly chilled at The French Laundry along with a side order of cold contempt for the taxpayers.

Your political instincts will distill this entire mess down to some brief talking points like, it isn’t your fault, or it wasn’t executed well, or we can do better, or we need more money, blah, blah, blah, or you’ll just blame Trump for everything.

I wonder if anyone has researched the mental health impact of long-term excessive exposure to Dippity-Do fumes. It appears that it may cause brain damage.

All snarkiness aside, I’m dead serious about the gas tax break.

P.S. While you’re at it, throw in an income tax break, a property tax break, a sales tax break, a payroll tax break, and a business tax break too. Heck, why not give us all the tax breaks all the way down the line? That would be great. This would put a lot of money back into the pockets of the hard-working people and businesses of this state to spend or save or invest as they see fit. You have the power to do it: Make it happen.